Fact Check: No correlation between CT hospital Medicaid share and profits

Connecticut hospitals have asserted that state Medicaid payment rates undermine hospital margins and force higher private plan rates. But the evidence doesn’t support the first assertion and is mixed on the second.

As in most states, Connecticut Medicaid hospital payment rates are lower than rates that commercial plans pay. It’s important to note that correlation is not causation. Hospital finances are complex and opaque. The interaction between factors and the influence of unmeasured factors are unclear.

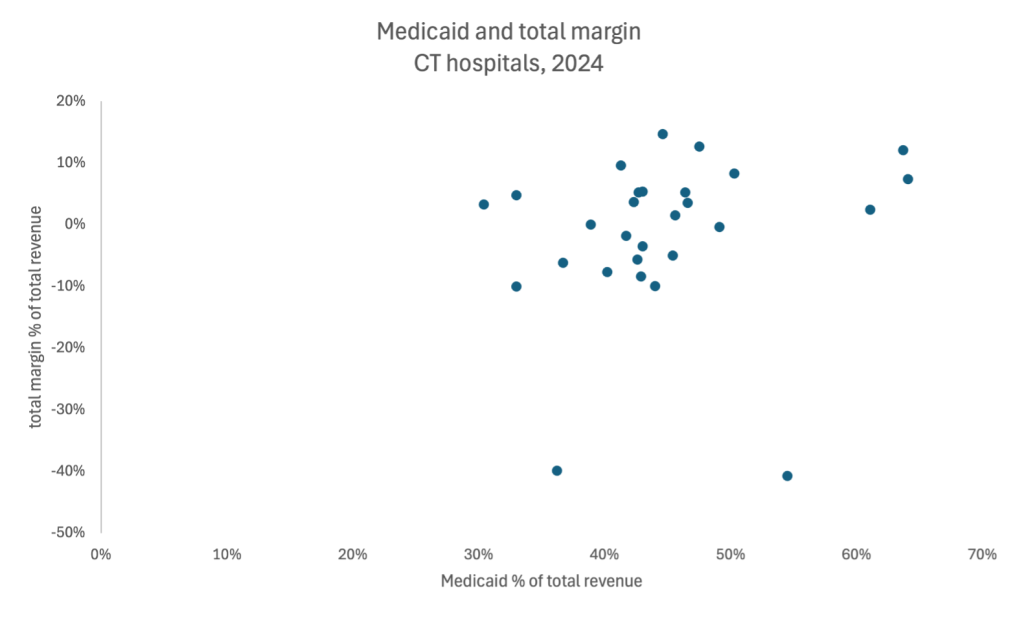

An analysis of data from the Office of Health Strategy’s (OHS) latest hospital financial report finds that, in 2024 the correlation between Medicaid’s share of total hospital revenue and total profits was 0.177, or negligible. The evidence does not support the assertion that hospitals with higher shares of Medicaid patients have lower profits or are less financially stable.

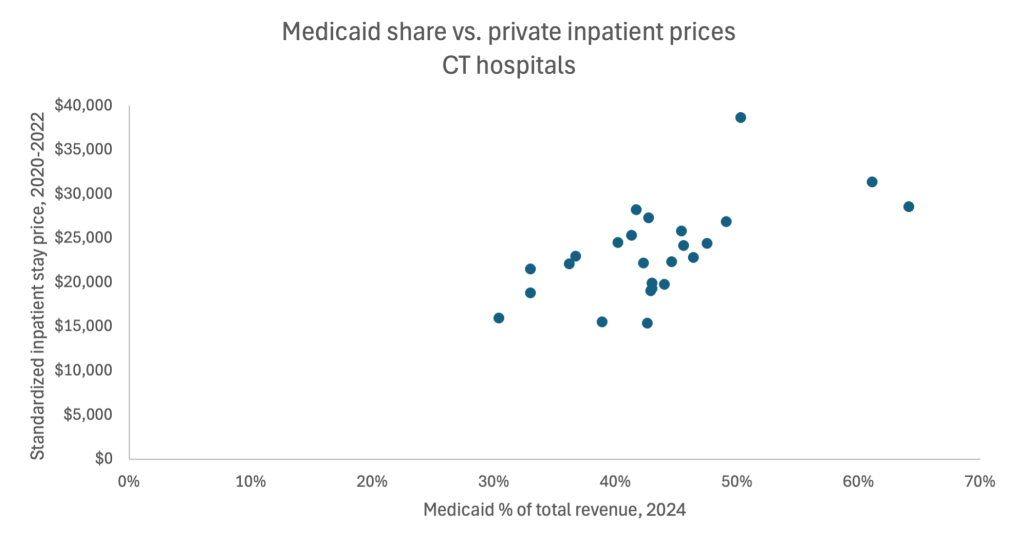

There is a moderate 0.613 correlation between Medicaid’s share of revenue (in 2024) and the standardized price of an inpatient stay paid by private plans (2020 to 2022) at Connecticut hospitals. This analysis compares OHS’s latest financial report with Connecticut hospital data from RAND’s latest analysis of hospital prices paid by private plans.

Nationally, there is little evidence that lower Medicaid, or Medicare, prices drive up prices for private plans on the national level. The same RAND analysis found that, “The relationship between a hospital’s share of its discharges from nonprivate payers [Medicaid and Medicare] and relative prices charged to commercial payers is not statistically significant.” In 2022, the Congressional Budget Office found that “the share of providers’ patients who are covered by Medicare and Medicaid is not related to higher prices paid by commercial insurers.”

Rather than Medicaid cost-shifting, there is overwhelming evidence that consolidation is the main cause of high healthcare prices. Hospitals with higher market power can demand higher prices, regardless of their Medicaid share of revenue. An analysis published in January 2025 by the federal Health and Human Services (HHS), Department of Justice (DOJ), and Federal Trade Commission (FTC) found that, “Empirical research unambiguously shows that hospital system-led acquisitions and mergers are associated with higher prices for services charged to insurers and patients.”

And contrary to hospital industry claims, consolidation does not result in higher quality or improved access to care. The RAND analysis found that “Despite higher prices, hospital consolidation has not been linked to either improved quality outcomes or to operating efficiency, and higher-priced providers often do not have higher quality than lower-priced providers.”